How a 1% Investment Fee Could Cost You Thousands (or Even Millions)

Why has no one told you this before?

Since starting this page, many people have approached me to review their investments. Financial advisers manage some of them, and others are invested directly in funds. To my surprise, most people have no clue about the fees they’re being charged or how damaging it is to their investment performance.

An annual 1% fee could mean 25% less value on your investment in 40 years. Read that again. Here’s a chart to let it sink in:

I also cover this blog in this YouTube video.

If you’re a regular blog reader, you will know I despise high investment fees. Because the fees aren't justified most of the time (actually, all of the time from what I have seen). Because high fees are usually associated with actively managed funds and we have enough research to know you likely won’t be better off in an actively managed fund in the long term. If you’re unsure what I’m talking about - see this video where I explain the difference between active and passive funds.

Why does no one tell me this?

No one is incentivized to warn you about fees on your investments, your asset manager or financial adviser definitely isn’t. Therefore it’s so crucial to educate yourself on this topic. 90% of my Instagram followers said they don’t know what fees they pay on their investments. I think this is because:

they don’t physically pay the invoices, the fee is automatically deducted from their investment

it’s notoriously difficult to figure out and understand the fees, and

the small percentages can be deceptive, 1% or 2% does not seem like much

You need to watch your own back

Two of the biggest shocks I’ve had when it comes to fees on portfolios:

Funds of funds, where people are invested in a “fund of funds” - which attracts a fee - to be invested in another fund with a second layer of fees. Total fees I have seen, considering all layers can be more than 6%!

Having an adviser oversee your portfolio, when you've started working together 3 years ago and most of your money has not even been allocated to an investment - it’s still lying in a cash account. So an adviser is taking fees for holding your money in cash and you’ve missed out on a 28.65% return over this time (S&P500 return from August 2021 to August 2024 with dividends reinvested, in USD)

Compounding is magic until fees spoil the potion.

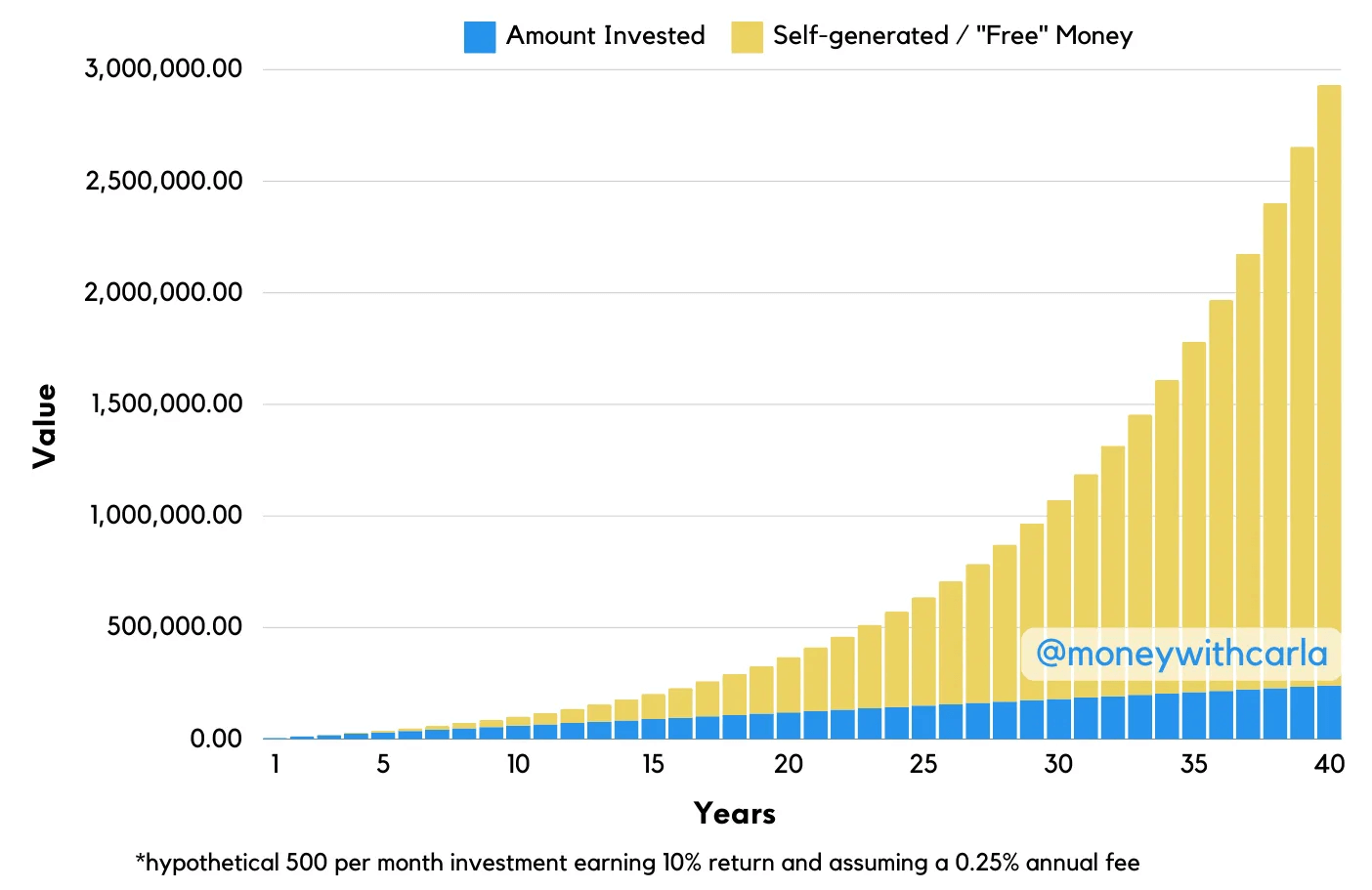

To understand the impact of fees on a portfolio, it’s important to understand the compounding principles behind growth. The chart below assumes 500 per month invested at a 10% return, whatever currency. Notice the exponential growth of money over time. The blue part of the chart increases linearly over time, as the cumulative amount of contributions adds up. The yellow part has an exponential line, which is achieved when money is reinvested and returns are earned on returns - this is labeled “Self-generated” or “Free Money”.

Now, if you add fees to this chart. Just a 1% fee, this is what it looks like (image below). The red part shows the growth you miss out on by paying annual fees on your portfolio. The fact that you are reinvesting less than the person above, means your investment is compounding less over time. And in the long term, the impact is significant.

And this is just a 1% fee. From what I’ve seen, fees hardly ever stop at 1%, they usually are closer to 2% all-in (adviser and total investment charges). This is how much each extra 1% means to you in “lost value”:

To make this even clearer and easier to interpret, these pie charts show how much potential value is lost by each incremental increase (image below).

1% fee means 25% of the value lost

2% fee means 44% of the value lost

3% fee means missing out on 58% - that’s more than half of the potential value.

A 3% fee is more common than you think -1.5% to an adviser and 1.5% to the fund is a total all-in fee of 3%.

Do you pay for performance?

Like with expensive cars or clothes, people sometimes perceive higher fees as higher value or better performance. This is categorically incorrect. Of course, you want to invest using a reputable firm or broker, but higher fees don’t add much value to you in the long term, it does the opposite - erode value.

I researched and mapped the performance of 5 funds to their fees in the chart below to illustrate this point. You will notice a very clear correlation between fees and returns. In plain language: The higher your fees are, the lower your returns will (very likely) be.

Please don’t make the mistake of thinking higher fees are ok because your investment will perform better. In the long term very, very few funds will beat the market (index funds). Morningstar data shows only 3% of funds beat the equivalent index over 15 years. I believe this will reduce closer and closer to 0% as the data’s timeline increases to 30 or 40 years.

How to identify these fees

Advisory fees - Your advisor should be able to send you a statement highlighting their fees, but from what I have seen it’s typically not easy to identify. It should be stated in the contract/agreement you signed with the adviser. If you cannot figure out the fees, contact your advisor and ask them what % they charge on assets under management (investment value).

Fund Management Fees - Depending on the country the fund is domiciled in (where it’s “hosted”), funds are generally required to report their fees in a regulated way. The most common is reporting fees on a “Fund Fact Sheet” which should be publicly available.

To identify the fees on the fund look for words like:

Total Expense Ratio

Total Investment Charges

Advice fee (if you use an advisor this is usually added to the costs above)

In my YouTube video, I also include a few screenshots of what to look out for on the fund documents to identify the fees.

This paid blog includes resources to help you identify if your fees are high.

How can you save on fees?

The first step is to understand the fees you’re paying. Spend some time to look into this because it could mean millions by retirement. Then, understand how you can save on fees by being a passive investor - read my blog Investing101 to learn more about this. Unfortunately, because passive funds do not attract a lot of fees, there is not a lot of incentive for advisers to push the product. Therefore, it’s crucial to educate yourself on this topic. I will also launch a Masterclass on this, sign up for the waitlist if you’re interested in joining.

Must fees fall?

This might sound like a 'Fees Must Fall' article, but my aim is to encourage you to understand that many investment products charge you for something you're not actually getting. It's like thinking you've bought a Ferrari, only to realize you're paying a Ferrari price for a souped-up Ford Focus painted in Ferrari red. A fund that promises superior returns for a high fee often won't pay off in the long term. So, the real question is: what are you paying these high fees for.

Link to my YouTube video covering this blog:

Disclaimer: My content is not personalized financial or tax advice but rather for educational purposes. I have made every effort to ensure accuracy but it cannot be guaranteed. Do your own research before making investment decisions.