How Strong Are Your 3 Wealth Pillars?

I've realized there are two main categories of reasons that hold people back from building wealth:

They could be committed to regular investing, but they’re investing in the “wrong products”. I attribute this to a lack of knowledge.

I have many examples of these, like Ashley, a 35-year-old mom diligently investing, every month, in a product for her 2-year-old son’s university education. And the fees are more than 3% all-in. It’s a shame when I come across this because she has all the right intentions and habits but she doesn’t know better.

2. They could know exactly how to be a smart investor, but they don’t have the best money habits. I call this a lack of discipline or unhelpful behaviours.

For example, Olly, who did his MBA with me in Switzerland and now earns a chunky salary in a corporate job in Zurich. He spends all his money on travelling and restaurants. He knows exactly which investments he should be making but his money behaviours are not healthy.

Ultimately, we want to achieve long-term compounding, and this is dependent on three factors:

Time (the longer you’re invested, the more compounding counts in your favour)

Returns (the more returns you earn, the more your money compounds)

Capital invested (regular investments, and increasing your capital contributions)

This inspired me to design the "Triangle Of Wealth." Without strengthening the two foundational components - knowledge and behaviour - the triangle can’t be strong enough to achieve the ultimate goal: compounding wealth.

Compounding

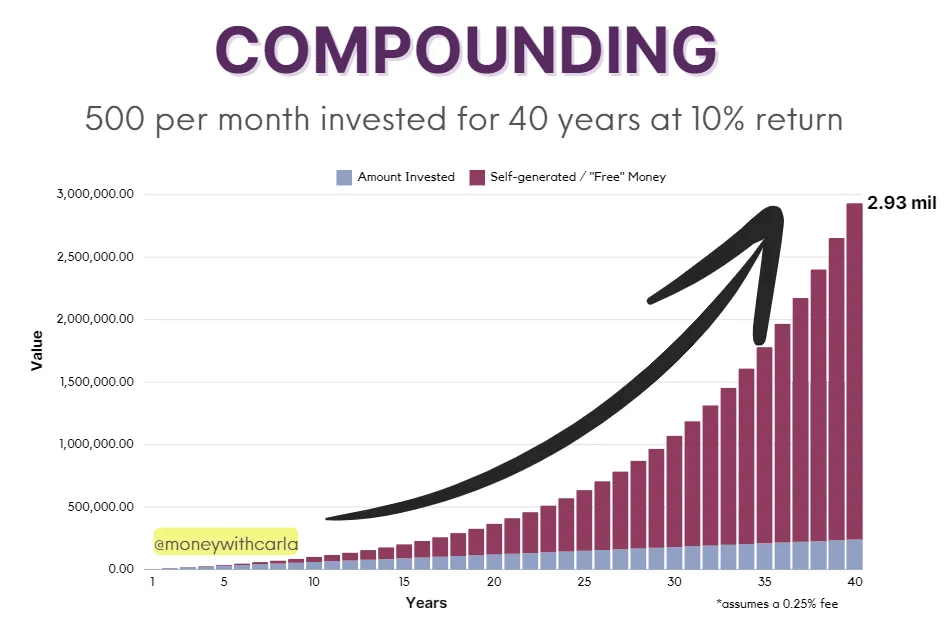

Compounding is at the top of the triangle. This is the single most underrated factor in building wealth. Warren Buffett calls compounding “the greatest force in nature,” and the image below shows why it’s so crucial. In the early years of investing, it’s hard to feel the impact of compounding, but by year 20, returns generated by previous (reinvested) returns often exceed the total amount initially invested. Notice how the blue part of the chart (amount invested) increases linearly, while the “self-generated” part—returns earned on returns—grows exponentially.

Thinking long-term about money is essential but one of the hardest mindset shifts to make. I don’t look at money invested today for what it is, but rather for its potential 20–30 years down the line. And that’s why I avoid touching that money now at all costs.

Discipline & Behaviour

A crucial component of smart investing is our behaviour toward money. Do you realize that wealth is built by money invested, not spent? Do you prioritize investing over impressing friends or social media followers? Do you have a monthly budget allocation for investing, so it becomes a fixed cash flow rather than an optional one?

Discipline also means developing the right attitude toward stock market risk and volatility. Becoming comfortable with stock market ups and downs can take anywhere from 1 to 5 years. That’s why I encourage starting small as early as possible. Over time, you’ll build confidence, adapt to the volatility, and no longer fear the stock market. I also encourage parents to talk to their kids about investing early on—exposure at a young age can mean they’re less fearful of market volatility when they begin investing their own money.

Knowledge

In a best-case scenario, smart investors take control of their investments, knowing it’s as simple as owning a few diversified, low-cost ETFs. In a worst-case scenario, I see young investors paying high fees to advisors and being invested primarily in low-risk, low-return products (like bonds or money market funds). In this blog, I explain why taking on enough equity risk is essential.

Self-education (building your own knowledge) is crucial to ensure you’re investing in a low-cost, diversified way. High fees can be hugely detrimental to growth, I explain how bad it is in this blog . Financial advisors often sell products with high fees because they have limited incentives otherwise. Therefore, it’s important to know what’s best for you before speaking with an advisor, so you can say “no” to something that doesn’t serve you well.

For some, working with an advisor makes sense. Take my father, for example. He works hard as a radiologist, including nights and weekends for emergencies, leaving no extra time to focus on his investments. Or my friend, a professional athlete, who makes good money but doesn’t feel confident managing her portfolio and is laser-focussed on her training and travels a lot. I’ll dedicate a separate blog to discussing who might benefit from using an advisor and who might not. Subscribe if you’re interested in reading this.

Knowledge also means addressing “home-country bias”—investing mainly in companies from your home country. Consider the size of the global stock market: the U.S., for instance, comprises over 40% of global capital markets. If at least 40% of your investments are not exposed to the US market, are you truly diversified?

I have good news to share: I’m working on something to give you the confidence to become a global, stock market investor. Sign up for my masterclass waiting list, to be notified when it launches: https://www.moneywithcarla.com/masterclass

In other news, I hosted my first Money with Carla event in Cape Town on 9 November and I spent a decent amount of time discussing the wealth triangle discussed in this blog. In my recent YouTube video, I share an extract of the event: Watch it here